Building A1 DDP - Dubai Silicon Oasis

Industrial Area - 342001 -

Dubai - United Arab Emirates

+971 50 756 2346

SERVICES

COMPANY LINKS

SIGN-UP

For Newsletter

The Middle East market is ready for rapid change in fintech payments since COVID gave quite a strong push. ‘Research and Markets’ data suggests that MEA consumers are keen in adopting digital payments and even trying new emerging ways such as cryptocurrency, biometrics, QR code – point is, they are fast, secure and contactless.

Almost half of the population of this region comprises youth and they like using smart screens and are preferring digital payments over traditional old-fashioned cash payments.

In this blog post, we are covering fintech payments in the Middle East market, digital wallet development features, timeline and cost.

Fintech payments refers to financial technology usage for making payments and what comes straight to our minds are the systems like PayPal, Apple Pay, Paytm, Payoneer, Amazon Pay, Google Pay, Transferwise etc.

Now what does fintech cover? Online payment systems, retail banking, education, fundraising, investment management, cryptocurrencies management to name a few.

Digital wallet is another significant aspect of fintech payments, e-wallet has eliminated the need of having physical wallets or keeping the plastic money. You just need to have a mobile phone with a digital wallet app for making all sorts of payments. Use your debit or credit card virtually or as we call them ‘virtual cards’. Secure virtual card solutions are becoming increasingly popular, offering the flexibility and protection that modern fintech users expect in digital transactions.

Even before COVID, digital payments were rising high in the Middle East and there was an increase of 9% from 2014-2019 compared to Europe’s average growth of 4-5% in total.

This data shows us that consumer preferences started changing before COVID as many of us give credit to pandemic for this digital adoption but that was so not the only case.

Now, people are adapting to the ‘new normal’ and changing the way they consume products and learn new skills.

Consumers of the Middle East market weren’t easily convinced that they can rely on digital payments but they were convinced enough that the next digital era is all about selling and buying online. They started changing their habits.

One significant factor here is the usage of social media by youth mostly. This has also led to an increase in online buying and selling commodities.

Do you know nearly 3 out of 4 (73%) consumers in the Middle East and Africa shopped more during the pandemic than before, according to a study by Mastercard, UAE.

Most consumers have found their sellers from Facebook (70%) and Instagram (59%). This shows the rise in social media usage and spending habits.

Overall, 73% of MEA (Middle East and Africa) consumers say that they shopped online since the COVID-19.

With the regulatory changes introduced in Saudi Arabia during 2019 and the UAE in 2021, there is a shift in the Middle East payments market.

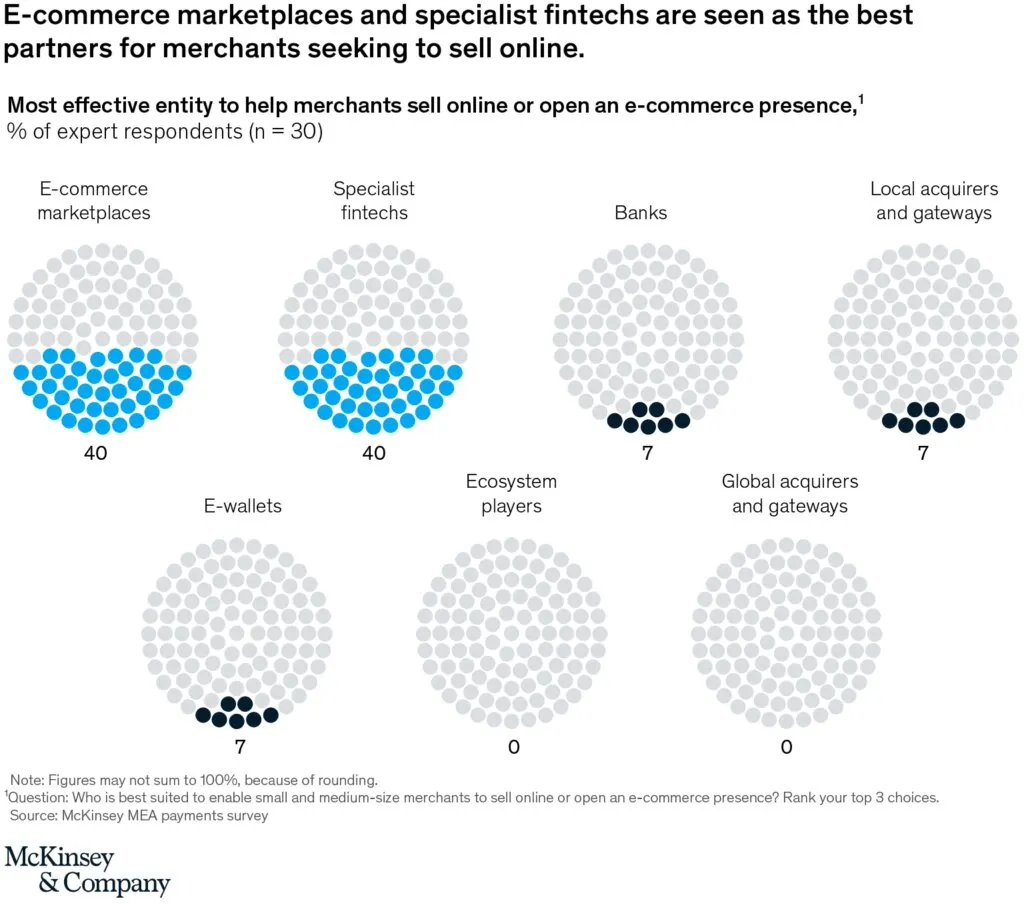

When McKinsey asked respondents in a survey about which institution would cause more impact on payments in the future, 40% ranked banks or bank-backed wallets and telecom company wallets as the second most popular choice.

Survey respondents say they will prefer to establish eCommerce store with fintech specialists or marketplaces.

Open banking is a kind of a regulatory reform where banks have to share consumer’s financial data (with consent) to other banks/authorized financial service providers.

The Middle East region is making reforms in open banking. According to the McKinsey report, 27% of the financial respondents say that regulatory approval for open banking will help consumers in digital payments.

Cross-border payments are another significant factor in fintech payments of the Middle East region. Real-time settlements between countries and scaling up on digital money transfer operations are some key factors for cross-border payments promotion.

McKinsey surveyed payment practitioners on ‘the future of payments in the Middle East’ revealed that almost half of the consumers enjoy safety, convenience and added value because of digital payments.

Moreover, the consumers interviewed said that they will never revert back to cash due to their flawless experience.

Secure digital payments help business owners reduce per transaction cost and from the consumer’s point of view, the systems are secure and protected against unauthorized access.

Carrying cash all the time is risky while on the other hand digital payments are seamless, convenient, and can easily be tracked.

The consumer can track his or her order from order placement till delivery. And digital payments take a few seconds literally.

Digital wallet is an online payment tool mostly in the form of an app where users can store virtual versions of debit and credit cards.

This way the user doesn’t have to enter details every time he purchases. Also digital wallets eliminate the need to carry physical wallets for making payments.

1-Closed wallets – companies selling products or services can develop a closed wallet for their customers. They can use their wallets for buying stuff, cancellations, returns, / refunds stored inside their wallets. Amazon Pay is one good example here.

2-Semi-closed wallets – users are allowed for payments from listed merchants/stores. Merchants agree with the user terms and sign onboarding agreements. Paytm is one such example.

3-Open wallets – mostly such wallets exist between banks. These wallets do all the functions of a semi-closed wallet, moreover funds can be drawn using ATMs.

On average, development of a digital wallet app takes 2-3 months.

Development cost of a digital wallet app depends on the types of features integration.

Basic mobile wallet app – $20,000 – 60,000.

Advance mobile wallet app – $85.000 – 200,000.

After the onset of COVID, online shopping doubled from 2020 and 2 major countries in the region are UAE and Saudi Arabia – secured 70% of the market size in the Middle East (by Research and Markets). We noticed consumer preferences, pandemic affect and business reforms as a positive sign of change in digital payments adoption.

Are you thinking of developing a digital wallet app but not sure how to start? Reach our business team, they can brainstorm with you and guide you the right way.

Nabeela is a content writer with 5+ years of experience in digital content and marketing strategy. Her articles have helped brands improve engagement by 2x and rank higher on search engines.

Her writing turns complex ideas into engaging content that resonates with the right audience. She focuses on creating articles that inform, inspire action, and support business growth.