Building A1 DDP - Dubai Silicon Oasis

Industrial Area - 342001 -

Dubai - United Arab Emirates

+971 50 756 2346

SERVICES

COMPANY LINKS

SIGN-UP

For Newsletter

Digital transformation in insurance is the process of using advanced technologies like AI, cloud, IoT, and data analytics to modernize operations, streamline workflows, and improve customer experiences.

By promoting technologies such as artificial intelligence, cloud platforms, IoT, and data analytics, insurers are moving from traditional, manual processes to agile, customer-centric operations.

The urgency is clear. Policyholders today expect the same seamless, personalized experiences from their insurers that they already receive from banks, e-commerce platforms, and travel booking sites.

They want mobile-first interactions, real-time updates, and self-service options, and they’re quick to switch providers if those expectations aren’t met.

The insurance sector is being reshaped by powerful forces, making digital transformation services in insurance more critical than ever.

At the center of this change are shifting customer expectations.

Competitive pressures from insurtechs and digital-first insurers are intensifying. These agile players are supporting digital transformation solutions such as AI-driven underwriting, self-service portals, and usage-based insurance models to capture market share quickly.

Their ability to innovate faster and deliver superior service forces traditional insurers to rethink their own digital transformation roadmap.

Ultimately, the success of digital companies and initiatives is measured by their impact on customer loyalty, trust, and profitability.

Insurers who embrace a structured digital transformation framework gain not only a competitive edge but also stronger customer relationships, more accurate risk management, and long-term growth potential.

The insurance industry is evolving rapidly under the influence of several converging forces.

These pressures and trends make digital transformation initiatives not just optional, but essential for insurers that want to stay competitive.

Today’s policyholders are more digital-savvy than ever. They expect self-service options, real-time interactions, and personalized policies that fit their lifestyles.

If these expectations are not met, customers are quick to switch providers.

Research shows that delivering an excellent digital experience can boost future adoption of digital channels by over 90%, proving that customer expectations are directly tied to retention and satisfaction.

The rise of artificial intelligence, machine learning, cloud platforms, and IoT has opened new possibilities for insurers.

These digital technologies enable smarter risk assessment, faster claims processing, and more efficient customer interactions.

Predictive analytics and big data are especially transformative, helping insurers detect fraud, automate repetitive tasks, and personalize offers at scale.

Insurtech startups and digital-native insurers are raising the bar with innovative, low-cost, and customer-centric business models.

By embracing advanced technologies and new digital tools, they are capturing market share from traditional carriers.

To survive, established insurers must embrace digital transformation to modernize operations and keep pace with these disruptive entrants.

Regulators are tightening requirements around transparency, data security, and customer protection.

Digital workflows and automation help insurers embed compliance into everyday processes, reducing human error and ensuring accountability.

For many organizations, regulatory change is both a challenge and an opportunity to modernize outdated core systems.

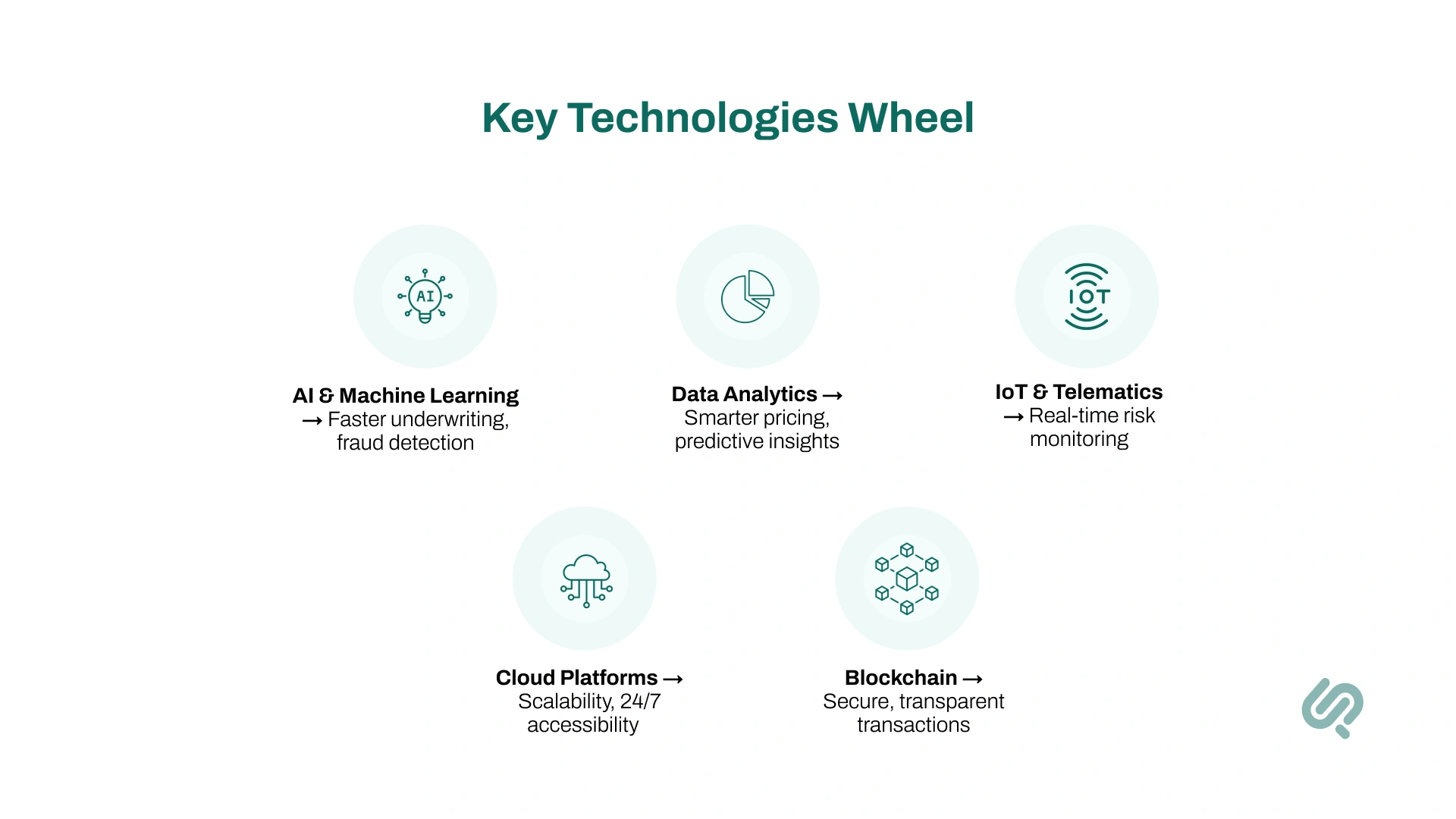

The heart of digital transformation in insurance lies in how insurers adopt and integrate new digital technologies. These tools are reshaping core operations, driving efficiency, and enhancing the customer experience.

AI and machine learning are among the most powerful drivers of digital transformation for companies

Data analytics is the backbone of every digital transformation framework.

An EY study found that 55% of insurance executives believe data and analytics will deliver the most value in the next few years. (1)

IoT and telematics create new opportunities for insurers to design tailored solutions and improve risk management.

Cloud platforms and mobile applications are essential for insurers looking to modernize their core systems.

Though still emerging, blockchain and smart contracts hold transformative potential.

Blockchain offers insurers an opportunity to build trust, reduce disputes, and accelerate claims, all critical to improving customer satisfaction.

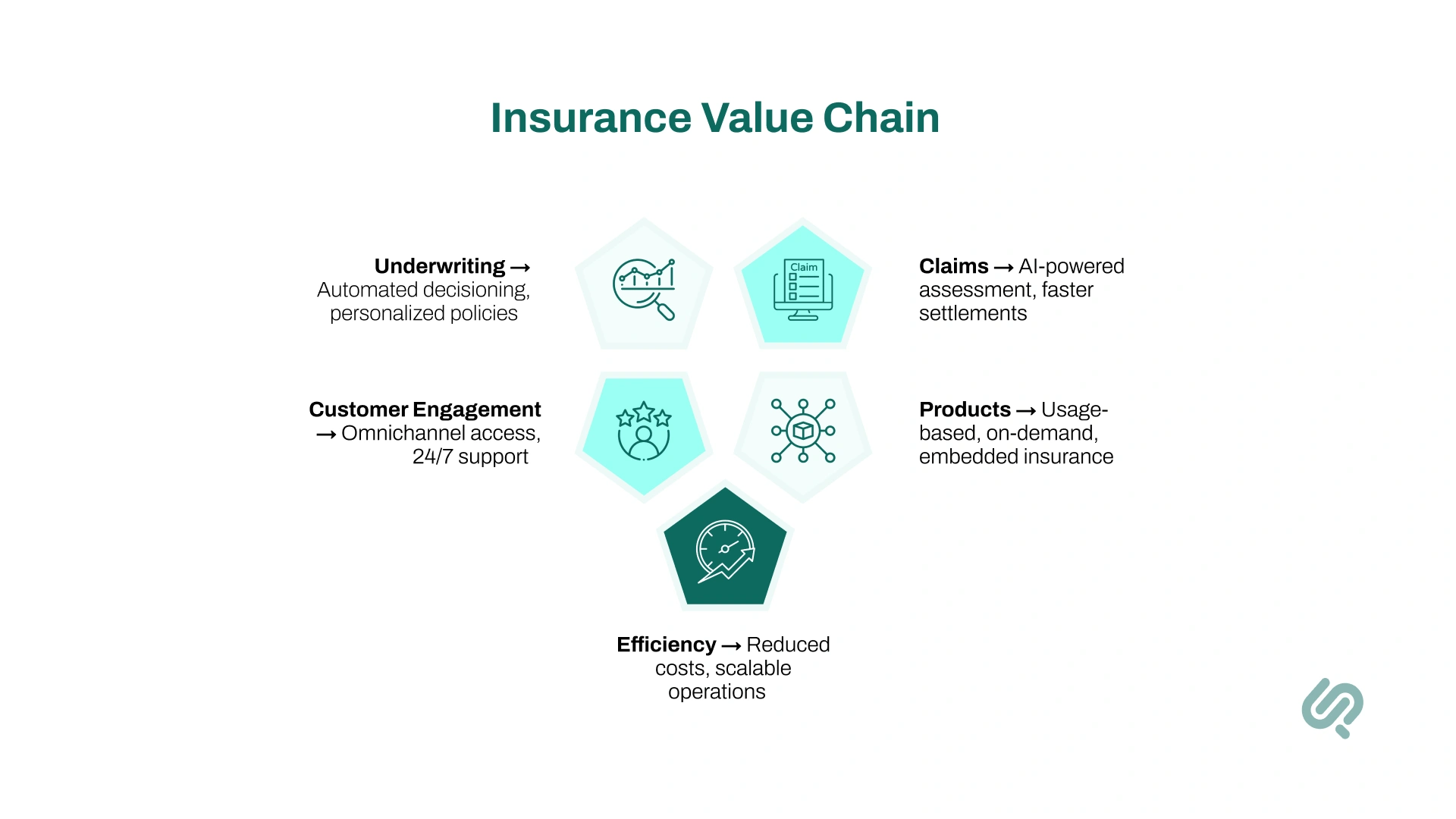

Digital transformation is reshaping the entire insurance value chain.

By modernizing underwriting, claims, customer engagement, product distribution, and internal operations, insurers are shifting from paper-heavy, manual processes to agile, data-driven systems that deliver efficiency and better customer experiences.

Underwriting has traditionally been slow and prone to bias. With new technologies, insurers can evaluate risk faster and more accurately.

Claims are often called the “moment of truth” for insurers, and technology is making this process faster and more transparent.

Insurance relationships extend far beyond policy purchase. Ongoing engagement is key to retention, and digital tools make it easier.

Technology is driving innovation, enabling insurers to go beyond traditional one-size-fits-all products.

Behind the scenes, technology is transforming insurers’ back offices, making them leaner and more scalable.

The adoption of digital transformation in insurance brings a wide range of measurable advantages.

From improving efficiency to building cultural agility, these benefits show why so many insurers are making technology adoption a top priority.

Automation of tasks like policy updates and claims intake reduces manual work, lowers errors, and speeds up workflows. Digital-first carriers now run at 10–15% expense ratios, compared to 25–35% for traditional players (3)

Ping An’s P&C unit, for example, boosted profits 70.7% year-over-year after investing in AI-driven loss assessment.

Self-service portals, mobile apps, and AI chatbots make insurance more accessible and transparent. Predictive analytics adds personalization with timely reminders and tailored offers.

J.D. Power reports that 92% of customers with excellent digital experiences would reuse digital channels, proving CX directly drives loyalty.

Digital tools enable flexible products like usage-based insurance (UBI), short-term coverage, and embedded insurance sold via travel sites or e-commerce.

Embedded insurance alone is forecasted to hit 15% of global premiums (~$1.1T) by 2033, giving insurers new revenue streams and lower acquisition costs.

Big data, IoT, and machine learning improve risk models while catching fraud early.

With U.S. insurance fraud costing $308.6 billion annually, tools that flag staged or inflated claims are critical. Smarter risk management strengthens profitability and ensures fairer pricing for policyholders.

Cloud platforms and low-code systems let insurers launch products in weeks, not months.

This agility enables faster responses to new risks, such as rolling out cyber or mobility insurance, and helps carriers stay ahead of insurtech challengers.

Transformation utlizes a culture of agility. Teams adopt data-driven decision-making, agile practices, and continuous improvement.

KPMG notes that 80% of leaders view cultural change as vital to success, ensuring insurers can sustain innovation over time.

Let’s look at the top challenges for digital transformation in insurance:

Digital transformation in insurance is not a one-time project. It’s a continuous journey.

The coming years will bring disruptive technologies and new business models that will reshape how insurers operate, design products, and serve customers.

Generative AI is moving beyond simple chatbots into complex workflows. Insurers are experimenting with AI models that draft policy documents, simulate claims, and generate automated summaries for adjusters.

This reduces manual workloads, speeds decision-making, and improves accuracy. However, strong governance will be essential to manage bias, ensure compliance, and maintain customer trust.

Embedded insurance will expand well beyond travel and retail into mobility, connected devices, and subscription services.

Customers will increasingly encounter coverage bundled with the products and platforms they already use.

Analysts predict this model could grow to $1.1 trillion in global premiums by 2033, making it one of the fastest-growing opportunities in the sector.

With IoT devices and wearables becoming mainstream, insurers will gain continuous streams of customer data.

Telematics can track driving habits for usage-based auto insurance, while smart home sensors can help prevent property losses.

This evolution shifts insurers from reactive claims handling to proactive risk prevention, resulting in fairer pricing and stronger customer engagement.

The next wave of risk management will be powered by big data analytics. Insurers will draw on external sources from credit scores to social behavior to refine risk models and detect fraud.

Rising climate risks and cyber threats will also demand adaptive, data-driven products that protect profitability while keeping policies relevant.

Agility will define the leaders of the future. Cloud platforms and low-code tools will allow insurers to launch new products in weeks instead of months.

This rapid adaptability will help insurers respond to emerging risks, regulatory changes, and shifting customer needs. Those stuck on legacy systems will struggle to keep pace.

Technology alone won’t guarantee success. Insurers that build a culture of innovation, encouraging experimentation, data-driven decision-making, and agile ways of working, will thrive in a fast-changing environment.

As KPMG notes, cultural agility is as important as technology adoption in sustaining transformation momentum.

Digital transformation in insurance is no longer optional. It’s the foundation of future competitiveness.

By embracing AI, data, IoT, and cloud technologies, insurers can create faster, smarter, and more customer-centric operations.

The winners will be those who balance technology adoption with cultural agility, turning transformation into a lasting advantage.

Ameena is a content writer with a background in International Relations, blending academic insight with SEO-driven writing experience. She has written extensively in the academic space and contributed blog content for various platforms.

Her interests lie in human rights, conflict resolution, and emerging technologies in global policy. Outside of work, she enjoys reading fiction, exploring AI as a hobby, and learning how digital systems shape society.